Private Equity Enters the Mainstream

Private equity (PE) in Australia has long been the preserve of institutional asset owners and the ultra-high-net-worth (UHNW) community. Today, semiliquid evergreen structures and feeder trusts have broadened access for sophisticated Australian investors, while still offering the diversification and long-term return characteristics that make the asset class so compelling. As a result, Private Equity firms in Australia are on the radars of affluent retirees seeking growth beyond listed markets for the everyday investor, however, the majority of people are unaware of how to get started.

What Is Private Equity?

Private equity entails taking ownership stakes in non-listed companies through professionally managed funds. Put simply, Private Equity in Australia is the practice of specialist investment funds buying and actively growing unlisted Australian businesses to unlock value and deliver long-term returns for investors. General partners (GPs) deploy capital, add strategic and operational value, and ultimately crystallise gains via trade sale, secondary buy-out or initial public offering (IPO). The result is exposure to the engine room of economic growth—away from the volatility and short-termism of public markets. Due to this, Private Equity Firms in Australia have become a trusted partner for founders looking to accelerate expansion.

A Growing Opportunity in Australia

According to the Australian Investment Council, domestic private-capital assets surpassed A$139 billion in 2024. Key drivers include:

- Rising allocations from superannuation funds and SMSFs

- Robust demand for growth-capital and mid-market buy-outs

- Strong track records from both local and global managers active in Australia

Typical strategy segments:

| Strategy | Primary Objective |

| Buy-outs | Control acquisitions of established businesses to unlock operational efficiencies |

| Growth Capital | Minority stakes in scalable companies seeking market expansion |

| Venture Capital | Early-stage investments in innovative business models |

Fund Structures: Evergreen versus Closed-Ended

One of the most significant shifts in the private equity landscape is the rise of evergreen (open-ended) fund structures. These funds allow investors to enter and exit periodically, offering continuous exposure to multi-vintage investments—unlike traditional closed-ended funds, which lock investors in for 7–10 years, or a direct co-investment which has no set exit maturity. Due to this, many private equity firms have embraced the evergreen model to cater to the liquidity preferences of their high-net-worth investors, which is different to that of institutional investors who are more absolute return focused.

Table 1 – Comparison of Private Equity Investment Structures

| Feature | Closed-Ended Fund | Evergreen (Open-Ended) Fund | Direct Co-investment |

| Liquidity | Locked-in, with infrequent distributions | Periodic entry/exit options | Locked in however with tag along or drag-along rights and the ability to sell within shareholder group. |

| Vintage Diversification | Single-vintage focus | Multi-vintage exposure | Single Transaction Focus |

| Capital Commitment | Capital called over time | Fully funded upfront | Fully funded on settlement, with possible further capital calls. |

| Valuation & Reporting | Quarterly or semi-annual | More frequent NAV updates | As needed. |

| Suitability | Experienced/wholesale investors | Broadening to retail investors | Professional / Wholesale investor only. |

Evergreen funds are particularly suited to high-net-worth individuals looking for more flexible access to private equity without compromising on diversification or long-term value creation. Our observations are that Private Equity Firms in Australia are using evergreen funds to try to reach scale faster than traditional vintaged vehicles.

Evergreen Fund Performance

Despite recent macro headwinds, many evergreen funds demonstrate strong long-term returns, with higher discrete annual returns compared to the closed ended vintages, but lower average annual returns of 10.88% to 8.55% compared to the closed ended funds with an average during the observation period of 11.35%. The differences could be put down to increased fees within the evergreen products compared to the closed ended vintages, or possible due to lower access to skilled Private Equity managers via evergreen funds compared to those of institutional grade closed ended funds.

Table 2 – Australian Evergreen Private Equity Feeder Funds

| Discrete Returns | |||||

| Fund Name | 2021 | 2022 | 2023 | 2024 | 2025 |

| Cordish Dixon – Private Equity Fund III | 56.70% | 44.90% | 28.16% | 18.76% | 16.96% |

| Barwon – Global Listed Private Equity | 18.38% | 16.22% | 27.08% | 18.52% | 12.92% |

| Fidante – Global Private Equity | 17.96% | 10.45% | 10.58% | 36.16% | 145.83% |

| Hamilton Lane – Global Private Assets | 5.51% | 5.29% | 4.62% | 3.95% | – |

| Partners Group – Global Value | 5.59% | 4.84% | 4.99% | 2.70% | 4.01% |

| PEP – Gateway Access | – | – | – | – | 5.15% |

| Schroder – Specialist Private Equity | 15.36% | 10.66% | 7.82% | 4.76% | 7.68% |

| Branford Castle – US Private Equity II | – | 10.89% | 12.48% | 11.69% | 35.48% |

| KKR – Private Equity (K-PRIME) (AUD) | – | – | – | 1.56% | 2.98% |

| Min | 5.51% | 4.84% | 4.62% | 1.56% | 2.98% |

| Max | 56.70% | 44.90% | 28.16% | 36.16% | 145.83% |

| Sector Average | 9.27% | 8.87% | 12.14% | 10.34% | 10.58% |

Source: FE Analytics (June 2025)

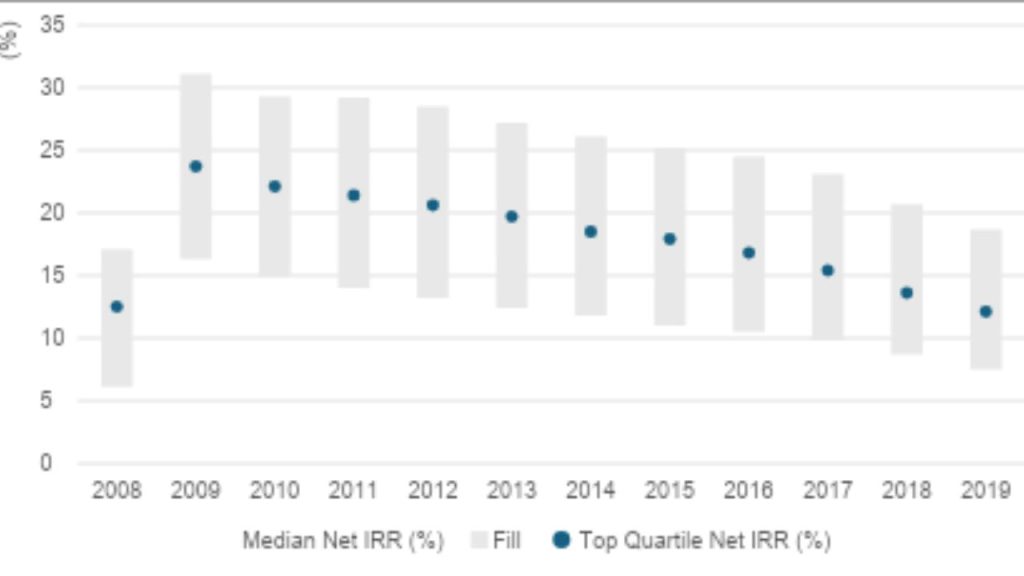

Closed-Ended Fund Returns by Vintage

Insights from Goldman Sachs’ 2024 ISG Outlook confirm that vintage year matters:

- Post-crisis vintages (2009–2011) saw outsized returns due to attractive entry valuations

- More recent vintages (2019–2021) have faced valuation compression and exit challenges amid rising interest rates

This trend supports the value of vintage diversification—a built-in feature of evergreen funds—which helps smooth performance and reduce timing risk over cycles.

In terms of the observations between, the average annual return has been 11.35% with maximums of 23.7% just after the Global Financial Crisis followed be declining positive returns after then.

Chart 1 – Net Internal Rate of Return (%) Distribution by Vintage Year

Source: Goldman Sachs

The dispersion underscores the importance of vintage diversification—an automatic feature of evergreen portfolios.

Co-Investments and Direct Deals

When investors participate alongside the lead GP on individual transactions, management fees often fall to zero and carried interest is typically waived. Academic evidence (Braun, Jenkinson & Schemmerl, 2020) shows co-investments perform in line with flagship funds when screening is robust. Benefits include:

- Fee compression of 300-500 bps

- Selective concentration into high-conviction sectors

- Immediate deployment, enhancing cash-flow-based performance metrics

Cashel syndicates thoroughly diligenced co-investments to eligible clients through a single managed-account wrapper.

Key Due-Diligence Considerations

- Illiquidity – secondary trades may incur 5-25 % haircuts in stress periods

- Minimum investment – wholesale thresholds often start at A$250 k

- Valuation methodology – prefer monthly, independent NAVs

- Leverage exposure – rising rates compress exit multiples; review covenants

- GP commitment – empirical sweet-spot is 5-10 % of fund capital

Why Fund Size Matters

Large pools can struggle to deploy capital efficiently. Global research finds IRR declines about 60 bps for every additional US $1 billion above US $5 billion in AUM (Rossi, 2023). Cashel therefore limits any underlying manager to A$10 billion.

Economic Impact

PE-backed Australian firms grew employment 5 % faster than non-backed peers between 2014-2023 (AIC Yearbook, 2024). Capital facilitates founder succession, ESG upgrades and regional export expansion—benefits that flow through to the wider economy.

Partner with Cashel Family Office

Cashel integrates evergreen, closed-ended and co-investment channels inside a managed-account platform, tailored to each client’s liquidity profile and tax structure. Explore:

Let’s Start the Conversation

Explore the possibilities of private equity in Australia and globally. Partner with Cashel to ensure your private capital strategy is informed, compliant, and aligned to your long-term wealth goals.

Get in touch

Phone +61 3 9209 9000 | Email : [email protected] | Join Cashel

Disclaimer: This content is intended for wholesale investors as defined under s761G of the Corporations Act 2001. Past performance is not a reliable indicator of future returns.

Further Readings

- Advising Australia’s Affluent Report (Praemium/Investment Trends)

- Australian Investment Council & Financial Standard. “Australian private-capital sector totals A$139 bn.” 2024.

- Braun, R., Jenkinson, T., & Schemmerl, C. “Adverse Selection and the Performance of Private-Equity Co-Investments.” JFE, 2020.

- Cashel Family Office. Alpha-Generating Investment Funds (White Paper), 2025.

- Franzoni, F., Nowak, E., & Phalippou, L. “Private-Equity Performance and Liquidity Risk.” RFS, 2012.

- Goldman Sachs (2024) – Investment Strategy Group Outlook

- GSAM (2021) – Private Equity Managers Pitchbook

- Rossi, A. “Private-Equity Fund Size.” SSRN Working Paper #4747628, 2023.